Any business in India that supplies goods or services with turnover exceeding Rs. 20 lakh (Rs. 10 lakh for North Eastern and hill states) has to get registered under GST.

1. What is GST Registration & why is it necessary?

Every business carrying out a taxable supply of goods or services and whose turnover exceeds the threshold limit of Rs. 20 lakhs (Rs 10 lakhs for North Eastern and hill states) is required to register as a normal taxable person. This process of registration is called GST registration.

For certain businesses, registration under GST is mandatory. If the organisation carries on business without registering under GST, it will be an offence under GST and heavy penalties will apply.

2. Who should get registered under GST?

Any business whose turnover exceeds the threshold limit of Rs. 20 lakhs (Rs 10 lakhs for North Eastern and hill states) will have to register under GST. Businesses registered under any of the pre-GST laws: VAT, Excise/Service Tax have to register under GST by default.

Apart from the normal taxpayer (as defined above), there are few special cases (as explained in section 3) that have to register for GST irrespective of their turnover.

3. Businesses that need to register under GST irrespective of their turnover

- Every person who is registered under the Pre-GST law (i.e., Excise, VAT, Service Tax etc.) needs to register under GST.

- When a business which is registered has been transferred to someone, the transferee shall take registration with effect from the date of transfer.

- Anyone who drives inter-state supply of goods**

- Casual taxable person

- Non-Resident taxable person

- Agents of a supplier

- Those paying tax under the reverse charge mechanism

- Input service distributor

- E-commerce operator or aggregator**

- Person who supplies via e-commerce aggregator

- Person supplying online information and database access or retrieval services from a place outside India to a person in India, other than a registered taxable person

**Latest Update:

As per 23rd GST Council Meet on 10th November 2017

E-commerce sellers/aggregators need not register if total sales is less than Rs. 20 lakh. Notification No. 65/2017 – Central Tax dated 15.11.2017

As per 22nd GST Council meeting of 6th October 2017

Service providers providing inter-state services are exempted from registration if their annual turnover is below 20lakhs (10 lakhs for Special states. 20 lakhs for J&K)

Notification No. 7/2017 – Integrated Tax dated 14th September 2017

Job workers making inter-state supply of services to a registered person are exempted from registration if their turnover is below 20lakhs (10 lakhs for Special states)

4. What are the documents/details required to register under GST?

PAN is mandatory to apply for GST registration (except in case of non-resident).

The document/details required to register for GST are:

5. What is the GST registration process?

Any business can get registered under GST by applying via the GST Online Portal or at GST Seva Kendra set up by the Government of India.

The Goods And Services Tax (GST) Registration services at ClearTax helps you to get your business GST registered and obtain your GSTIN.

Here is the step by step info-graphic on the registration process :

6. What is the fees applicable to register under GST?

Businesses can register for GST and obtain GSTIN free of cost.

7. What is the penalty for not registering under GST?

An offender not paying tax or making short payments (genuine errors) has to pay a penalty of 10% of the tax amount due subject to a minimum of Rs.10,000.

The penalty will at 100% of the tax amount due when the offender has deliverately evaded paying taxes

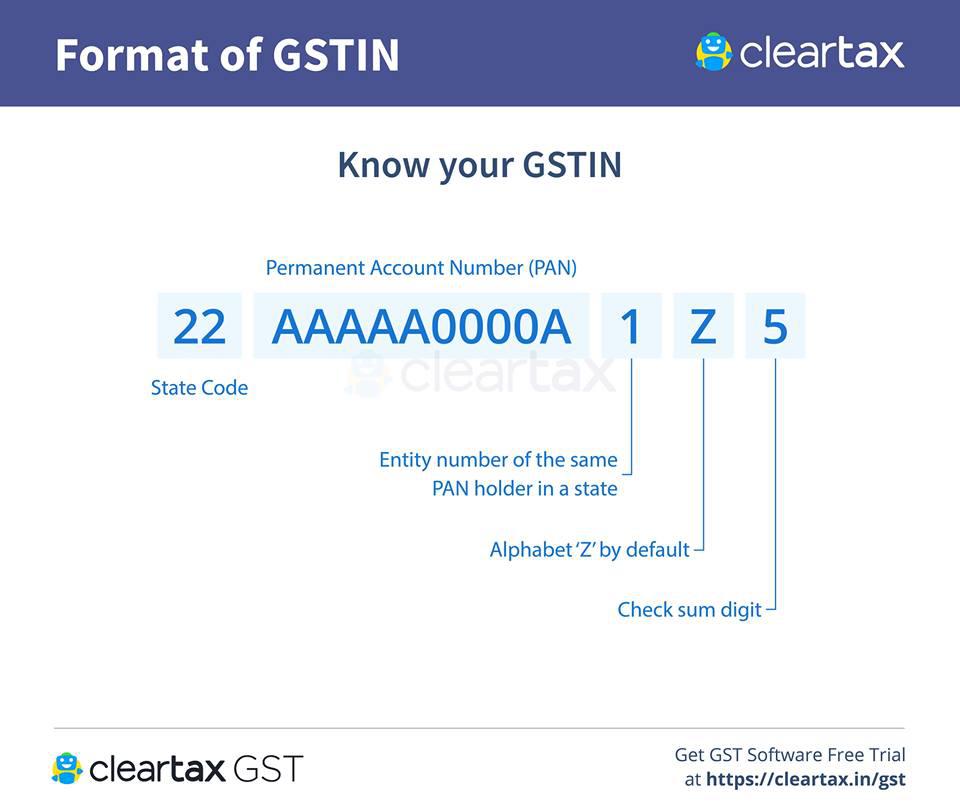

8. What is GSTIN?

All businesses that successfully register under GST are assigned a unique Goods and Services Tax Identification Number also know as GSTIN.

9. When should a business apply for multiple GST registrations?

If a business operates from more than one state, then a separate GST registration is required for each state. For instance, If a sweet vendor sells in Karnataka and Tamil Nadu, he has to apply for separate GST registration in Karnataka and TN respectively.

A business with multiple business verticals in a state may obtain a separate registration for each business vertical.

10. What is Composition scheme and when should a business opt for it?

Small businesses having annual turnover less than Rs. 75 lakhs can opt for Composition scheme.

Composition dealers will pay nominal tax rates based on the type of business:

- Composition dealers are required to file only one quarterly return (instead of three monthly returns filed by normal tax payers).

- They cannot issue taxable invoices, i.e., collect tax from customers and are required to pay the tax out of their own pocket.

- Businesses that have opted for Composition Scheme cannot claim any input tax credit.

Composition scheme is not applicable to :

- Service providers

- Inter-state sellers

- E-commerce sellers

- Supplyier of non-taxable goods

- Manufacturer of Notified Goods

11. Benefits of registering under GST

11.A. For normal registered businesses:

1. Take input tax credit

2. Make interstate sales without restrictions

11.B. For Composition dealers:

1. Limited compliance

2. Less tax liability

3. High working capital

11.C. For businesses that voluntarily opt in for GST registration (Below Rs. 20 lakhs)

1. Take input tax credit

2. Make interstate sales without restrictions

3. Register on e-commerce websites

4. Have a competitive advantage compared to other businesses

Thank you madam.

ReplyDelete